California-headquartered 23andMe Holding (ME) sells consumer genetic test kits. It is also engaged in drug research and is collaborating with GlaxoSmithKline (GSK) on a cancer drug discovery program.

Let’s take a look at 23andMe’s latest financial performance and risk factors.

23andMe’s Fiscal 2022 First-Quarter Results and Full-Year Guidance

The company reported a 23% year-over-year increase in revenue to $59 million for its Fiscal 2022 first quarter ended June 30. It posted a loss of $42 million, compared to a loss of $36 million in the same quarter last year. 23andMe ended the quarter with $770 million in cash. (See 23andMe stock charts on TipRanks).

23andMe said it advanced its therapeutics programs in fiscal Q2. Its immuno-oncology program with GSK is currently in Phase 1 clinical trial. The company further revealed that its wholly-owned immuno-oncology program is expected to be trialed before the end of March 2022.

For the Fiscal 2022 full-year, 23andMe anticipates revenue in the range of $250 million - $260 million. It expects to report a loss of $210 million - $225 million.

23andMe’s Risk Factors

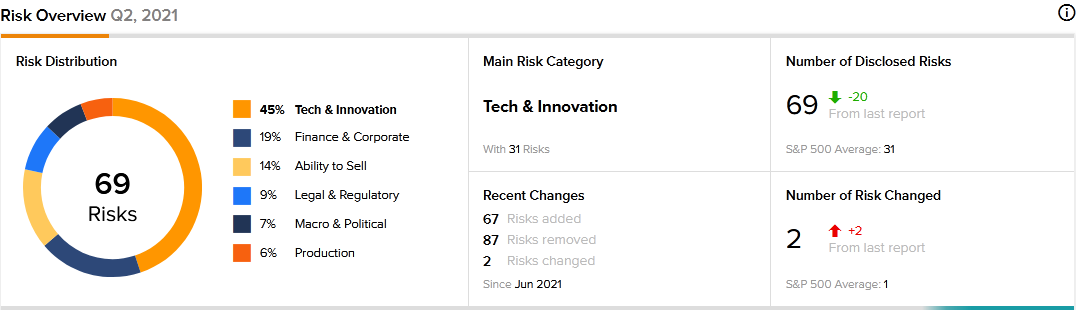

The new TipRanks Risk Factors tool reveals 69 risk factors for 23andMe. Since filing its Fiscal 2021 full-year report, the company has revised its risk profile to introduce 67 new risk factors.

23andMe tells investors in a newly added Financial and Corporate risk that it has a history of making losses and that there is no guarantee it will achieve profitability or remain consistently profitable. It further says that its ability to carry forward losses to reduce its future tax bills may be limited.

The company has also expanded its Tech and Innovation risk factors. It cautions investors that while it expects to invest more in its therapeutic business, it cannot assure that those efforts will be successful. 23andMe goes on to say that if its therapeutic efforts fail, its ability to expand and attain certain strategic objectives may be hampered.

Tech and Innovation is 23andMe’s top risk category, accounting for 45% of the total risks. That is above the sector average at 25%. 23andMe’s shares have declined about 24% since the beginning of 2021.

Analysts’ Take

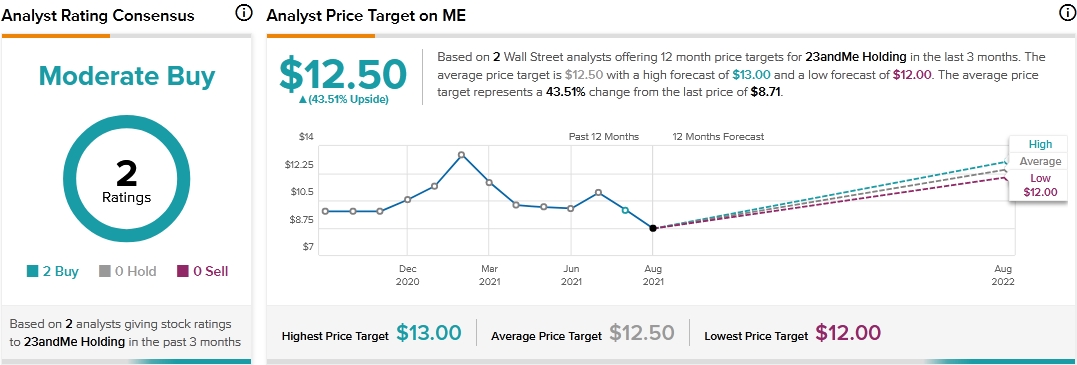

Credit Suisse analyst Tiago Fauth recently initiated coverage on 23andMe stock with a Buy rating and a price target of $13. Fauth’s price target implies 49.25% upside potential.

The analyst commented, “We believe 23andMe offers investors a platform that enables novel discoveries into the causes and potential treatments of a wide variety of diseases at unprecedented statistical power…In collaboration with its exclusive strategic partner GlaxoSmithKline, the company has identified over 40 novel drug targets and 19 validated targets…Looking beyond the GSK partnership, we see substantial optionality for ME’s Therapeutics segment over the long run."

Consensus among analysts is a Moderate Buy based on 2 Buys. The average 23andMe price target of $12.50 implies 43.51% upside potential to current levels.

Related News:

What Do Astra Space’s Earnings and Risk Factors Tell Investors?

Nvidia-Arm Deal to Face Another Investigation by Regulators

Paysafe to Acquire viafintech; Street Says Buy

The post A Look at 23andMe’s Earnings and Risk Factors Amid Therapeutic Efforts appeared first on TipRanks Financial Blog.

-----------------------------

By: Neha Gupta

Title: A Look at 23andMe’s Earnings and Risk Factors Amid Therapeutic Efforts

Sourced From: blog.tipranks.com/a-look-at-23andmes-earnings-and-risk-factors-amid-therapeutic-efforts/

Published Date: Mon, 23 Aug 2021 10:32:30 +0000

Read More

Make Money OnlineForexInvestingBitcoinVideosFinancePrivacy PolicyTerms And Conditions

Make Money OnlineForexInvestingBitcoinVideosFinancePrivacy PolicyTerms And Conditions